Running a small service business, whether you are a personal trainer chasing invoice payments or a beautician waiting on card settlements, means cash flow is never far from your mind. The role of Stripe payouts for small businesses goes well beyond simply receiving money. It shapes when you can pay suppliers, cover rent, or reinvest in equipment. Many owners assume that a completed booking equals money in the bank. It rarely works that way. This guide breaks down exactly how Stripe payouts work, what affects your timing and net amounts, and how to plan your finances around the reality of payout schedules.

Table of Contents

- How Stripe payouts work for small businesses

- Understanding available balance and settlement timing

- Payout schedules and funding methods

- Payout networks and global considerations

- Best practices for managing Stripe payouts as a small service business

- Rethinking payout expectations: what most small businesses miss

- Streamline your payments and scheduling with Nextro

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand payout timing | Stripe payouts move your money to your bank based on set schedules affecting your cash flow. |

| Monitor available balance | Available balance shows what you can withdraw and changes immediately with holds or authorisations. |

| Choose a payout schedule | Daily, weekly, or monthly payout options help match timing with your business cash needs. |

| Know your payout network | Domestic transfers like Faster Payments are faster and cheaper than international ones. |

| Use automation to stabilise cash flow | Configuring Stripe’s automatic payout schedules reduces surprises and supports steady income. |

How Stripe payouts work for small businesses

When a client pays you through Stripe, that money does not land in your bank account immediately. It moves through a sequence: the client's card is charged, Stripe processes the transaction, deducts its fees, and then transfers the remaining balance to your bank on a schedule you configure. Payouts represent moving the net amount from your Stripe balance to your bank account after fees, which matters enormously for businesses operating on tight margins.

For a personal trainer charging £60 per session, Stripe's standard processing fee of 1.5% plus 20p (for UK cards) means roughly £1.10 comes off the top. Multiply that across 20 sessions a week and you are looking at around £22 in fees weekly. Not catastrophic, but it adds up across a year, and it directly affects the net amount landing in your account. Understanding about Stripe payments before you set your pricing helps you build those costs in from the start.

Here is what happens at each stage of a Stripe payout:

- Transaction processed: Stripe charges the client's card and holds the funds.

- Fees deducted: Processing fees and any platform margins come off the gross amount.

- Funds enter your Stripe balance: The net amount sits in your Stripe account, not yet in your bank.

- Payout triggered: Based on your schedule, Stripe initiates a transfer to your bank.

- Bank settlement: Your bank receives the funds and makes them available, which can take an additional working day.

Each step takes time. Knowing this timeline prevents the unpleasant surprise of a shortfall when a bill lands before your payout does.

Understanding available balance and settlement timing

Your Stripe dashboard shows several balance figures, and confusing them is one of the most common mistakes small business owners make. The available balance is the only number that matters for payouts. It represents funds that are fully settled, net of any holds or pending authorisations, and ready to transfer to your bank.

The pending balance, by contrast, includes payments that have been collected but are still within Stripe's processing window. A card payment made today might sit in pending for two to seven days before it becomes available. Available balance fluctuates during the day due to holds and authorisations, acting as a guardrail against overdrafts. If you schedule a payout that exceeds your available balance, Stripe will simply not process it.

This matters practically. A beautician who takes ten bookings on a Monday, all paid upfront via card, might see £800 in their Stripe account by Tuesday. But if those funds are still in pending, the available balance could be zero. Attempting to pay a product supplier from that balance would fail.

Key things to watch on your Stripe balance:

- Available balance: Ready to pay out now.

- Pending balance: Collected but not yet settled; cannot be paid out.

- Reserved balance: Held by Stripe for potential disputes or refunds.

- Negative balance: Can occur if refunds or chargebacks exceed your available funds.

Pro Tip: Check your available balance the day before you expect a payout, not the day of. If a dispute or refund has come in overnight, your payout amount may be lower than anticipated.

Managing your Stripe balance proactively, rather than reacting to what arrives in your bank, is what separates businesses that feel financially stable from those that constantly feel behind.

Payout schedules and funding methods

One of the most useful things Stripe offers small businesses is the ability to configure your payout schedule. You are not stuck waiting for Stripe to decide when you get paid. You choose. The three main options are:

- Daily payouts: Funds transfer to your bank every business day. Best for businesses with high transaction volume or tight cash flow needs.

- Weekly payouts: Funds accumulate across the week and transfer on a set day. Good for businesses that prefer a single weekly income event to reconcile against.

- Monthly payouts: All settled funds transfer once a month. Suits businesses with low overheads and stable reserves who want to minimise bank reconciliation work.

Beyond frequency, the funding method affects how quickly money actually arrives. Payout timing depends on funding method: ACH transfers take roughly three business days, wire transfers can arrive the same day but carry additional fees, and automatic transfers from your Stripe payments balance follow whichever daily, weekly, or monthly cadence you have set.

Here is a comparison of the main payout methods available to UK small businesses:

| Method | Speed | Cost | Best for |

|---|---|---|---|

| ACH / BACS transfer | 2 to 3 business days | Low | Most small businesses |

| Faster Payments (UK) | Same day or next day | Low to none | UK domestic accounts |

| Wire transfer | Same day | Higher fees | Urgent or large transfers |

| Automatic scheduled | Depends on schedule | Standard processing | Consistent cash flow planning |

Small businesses can set automatic payout schedules to plan cash flow around predictable payout dates, which is particularly valuable when you have fixed monthly expenses like studio rent or equipment leases. Setting payout schedules to align with those fixed costs removes a significant source of financial stress.

Payout networks and global considerations

The network Stripe uses to transfer your funds is not something most small business owners think about. But it directly affects how fast your money arrives and what it costs to get there.

In the UK, Stripe uses the Faster Payments Service for eligible domestic transfers. This means money can arrive in your bank account the same day or within a few hours, at no extra cost. For a personal trainer or beautician whose clients are all UK-based, this is the default and it works well. Domestic networks like Faster Payments settle faster and cheaper than international transfers, which pass through intermediary banks and can take three to five business days.

Where this becomes relevant for small service businesses:

- Paying overseas contractors or freelancers: If you hire a remote social media manager or content creator based abroad, international payout delays affect when they receive payment.

- Operating across borders: Wellness professionals who run retreats or workshops in multiple countries may deal with currency conversion fees on top of transfer delays.

- Platform fees from international processors: If you use a booking platform based outside the UK, their payouts to you may route through international networks rather than Faster Payments.

Pro Tip: If you regularly pay anyone outside the UK, set up a separate Stripe account or sub-account for international transactions so you can track those fees and delays separately from your domestic income.

Stripe payout insights for UK businesses confirm that sticking to domestic bank accounts wherever possible keeps your payout process simple, fast, and low-cost.

Best practices for managing Stripe payouts as a small service business

Knowing how payouts work is only half the job. The other half is building habits that keep your cash flow predictable, even when client bookings fluctuate.

- Audit your payout dashboard monthly. Look at the fees deducted, any disputes held, and the difference between your gross income and net payout. This single habit catches problems early.

- Match your payout frequency to your expense cycle. If your biggest costs hit on the 1st of the month, set weekly payouts so you always have a buffer. Daily payouts sound appealing but can make reconciliation messy.

- Read the dispute and refund policy before you rely on Stripe. Chargebacks can freeze funds for weeks. Knowing this in advance means you keep a small reserve rather than spending every payout immediately.

- Use Stripe's automatic payout feature. Manual payouts require you to remember to initiate them. Automation removes that risk and creates a consistent, predictable income rhythm.

- Build a one-week cash buffer. Even with perfect payout scheduling, unexpected holds happen. A buffer of one week's operating costs absorbs those shocks without disrupting your business.

Reviewing dashboards for deductions and maintaining a predictable payout cadence are the two habits that most reliably prevent cash flow wobble in small service businesses.

Pro Tip: Set a recurring calendar reminder for every Monday morning to check your Stripe available balance and confirm your upcoming payout amount. Five minutes of checking saves hours of scrambling later.

For a practical walkthrough of accepting payments as a personal trainer, the process becomes much clearer when you see it mapped to a real business scenario.

Rethinking payout expectations: what most small businesses miss

Here is the uncomfortable truth most payment guides will not tell you: a strong revenue month does not guarantee a strong cash month. These are two different things, and conflating them is where most small service businesses run into trouble.

The assumption is passive: money comes in, money goes out, and the gap between them is profit. But payout timing, holds, disputes, and fee structures mean your available cash at any moment is almost always less than your earned revenue. Available balance is different from total earned, and payout cadence directly affects your working capital and cash flow stability.

Think of your Stripe payout schedule not as a delivery mechanism but as a financial management lever. A weekly payout on Fridays means you are making a deliberate decision about when cash enters your operating account. That decision should be made in relation to your rent date, your payroll date, and your supplier payment terms. Not chosen at random during signup.

Most small business owners pick a payout schedule once and never revisit it. But your business changes. A beautician who starts solo and grows to a team of three has completely different cash flow needs than she did eighteen months earlier. Revisiting your managing payout timing settings every six months is a simple act that can meaningfully improve your financial resilience.

The businesses that feel financially stable are not necessarily the ones earning the most. They are the ones who have aligned their income timing with their outgoing commitments. Stripe gives you the tools to do that. Most people just never use them intentionally.

Streamline your payments and scheduling with Nextro

Managing Stripe payouts is far easier when your bookings and payments live in the same place.

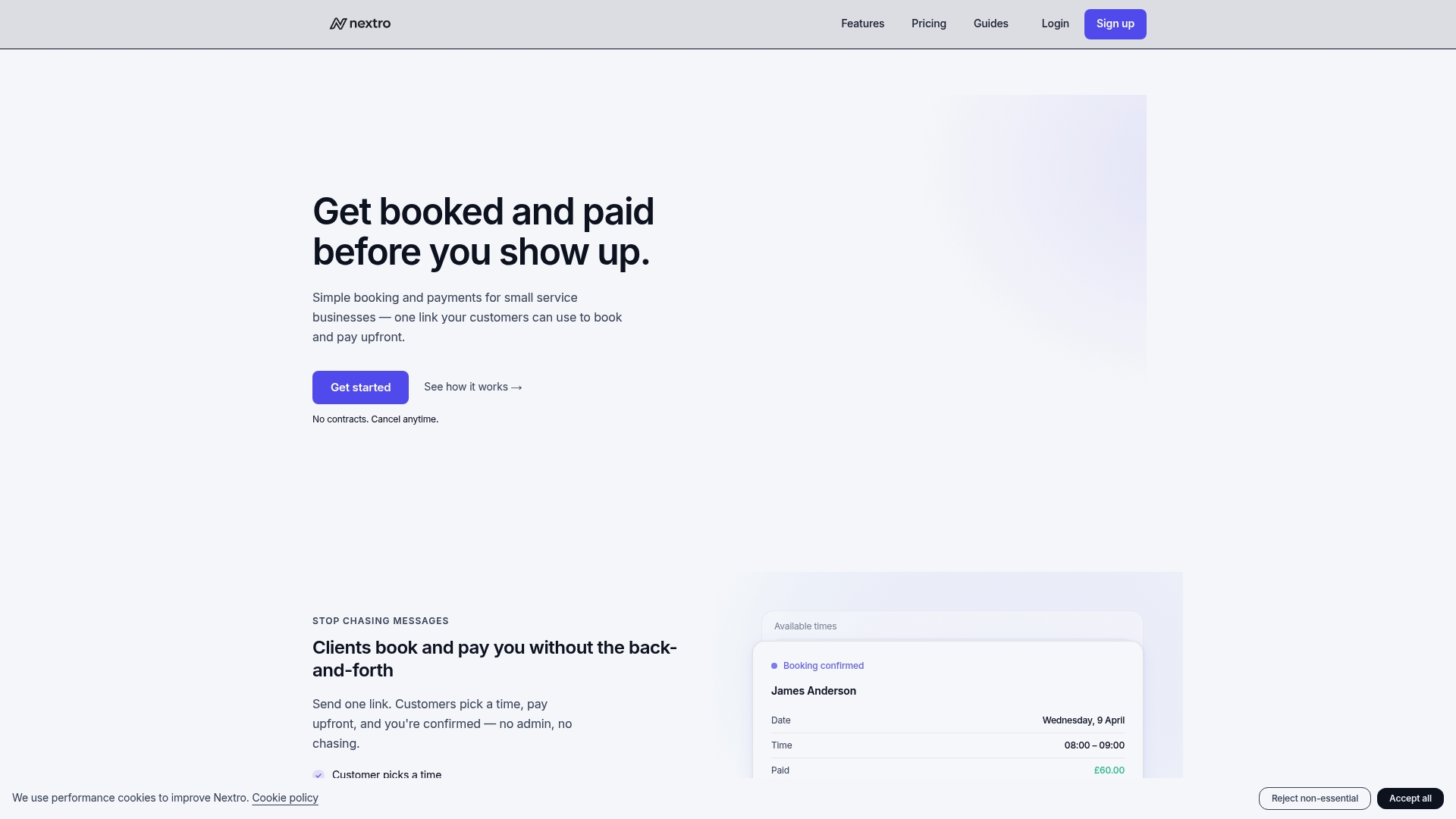

Nextro connects personal trainer Stripe payments and client scheduling into a single platform, so you can see exactly what you have earned, what is pending, and when it will arrive, without switching between tools. Clients book and pay upfront through your personalised booking link, which means your Stripe balance grows consistently and your payout schedule reflects real, confirmed income. Automated reminders reduce no-shows, and the platform's stripe payouts feature gives you clear visibility over your cash flow at every stage. For fitness and wellness professionals who want to stop chasing payments and start planning with confidence, automatic scheduling for personal trainers through Nextro is the practical next step.

Frequently asked questions

What is the difference between Stripe available balance and payout amount?

Available balance is the amount you can currently transfer to your bank, accounting for holds and authorisations, while payout amount is the net sum after fees actually sent to your bank. Available balance reflects funds minus holds, acting as a guardrail to avoid overdraft.

How does payout schedule affect my small business cash flow?

Choosing a consistent payout schedule, whether daily, weekly, or monthly, helps smooth income timing, avoid cash flow gaps, and plan expenses reliably. Scheduling payouts helps small business owners plan cash flow around expected payout dates.

Are payouts from Stripe instant?

No. Payout speed depends on the funding method and payment network. Faster Payments in the UK settle typically the same day, but traditional international transfers take longer due to intermediary banks.

How can I avoid unexpected deductions from my payouts?

Review your payout dashboard carefully before sign-up, understand all fees and dispute policies, and monitor deductions regularly. Unexpected deductions harm trust, and clear fee transparency before sign-up is essential.

Can I automate Stripe payouts for my small business?

Yes. Stripe lets you set automatic payout schedules, daily, weekly, or monthly, to fund your bank transfers automatically, simplifying cash flow management. Automatic payout schedules help move funds from your payment balance to your bank automatically.